Valuing Low P/E Stocks: Opportunities vs. Valuation Traps

For anyone walking the value-investing path, few numbers are as tempting as a low P/E ratio. A stock trading at 8x or 10x earnings feels like a clearance sale. The business is earning money, yet the market seems uninterested. Surely this is where fortunes are made?

Sometimes, yes. But just as often, low P/E stocks are cheap for a reason and that reason can quietly destroy capital. Understanding why a P/E is low matters far more than how low it is. Let’s slow down, strip away the noise, and look at low P/E stocks the way a patient investor should.

1. What the P/E Ratio Really Tells You

1.1. Core Definition: At its simplest, the Price-to-Earnings (P/E) ratio tells you how much the market is willing to pay for one rupee of a company’s earnings.

$$\text{P/E Ratio} = \frac{\text{Market Price}}{\text{Earnings Per Share}}$$1.2. Baseline Perception: A P/E of 10 means investors are paying ₹10 for every ₹1 the company earns. Traditionally:

Low P/E: Cheap, unloved, possibly undervalued

High P/E: Expensive, popular, growth expectations baked in

1.3. The Hard Reality: The uncomfortable truth most beginners learn the hard way is that the P/E ratio doesn’t tell you whether earnings will survive. And that’s where things get interesting and dangerous.

2. Why Low P/E Stocks Look So Attractive

Low P/E stocks pull value investors in because they promise asymmetry—limited downside, large upside. The thinking goes like this:

2.1. The business is already profitable.

2.2. Expectations are low.

2.3. Even a small improvement could re-rate the stock.

And sometimes, that thinking is spot on.

3. When Low P/E Stocks Are Genuine Opportunities

3.1. Market Overreaction

Markets are emotional creatures. Bad news—such as quarterly misses, regulatory headlines, or macro fears—often pushes prices down faster than fundamentals deteriorate.

In such moments, quality businesses can trade at low P/Es temporarily. Investors who bought strong banks or FMCG companies during crisis periods didn’t do anything clever—they simply stayed rational when the market panicked.

3.2. Cyclical Lows (Not Peaks)

Cyclical businesses move in waves. Steel, oil, chemicals, and automobiles see profits swing wildly based on economic conditions.

A cyclical stock trading at a low P/E during a downturn can be a gift, because earnings are depressed, not inflated. Timing matters here. Buying cyclicals at the bottom of the cycle is value investing. Buying them at the top is how people get trapped.

3.3. Boring but Predictable Businesses

Some businesses never make headlines. They don’t promise disruption or exponential growth. Yet they quietly generate cash year after year.

Utilities, consumer staples, and mature retail chains often trade at modest P/Es simply because they’re boring. Over time, dividends and steady compounding do the heavy lifting.

4. How Low P/E Ratios Fool Investors

Now for the harder part. Many low P/E stocks aren’t bargains—they’re warnings. Here’s how they fool even experienced investors.

4.1. The Cyclical Peak Illusion

This is one of the most common traps.

4.1.1. A cyclical company reports record profits.

4.1.2. Margins expand dramatically.

4.1.3. EPS shoots up.

4.1.4. P/E collapses.

4.1.5. The stock suddenly looks cheap—but earnings are at their peak, not normal.

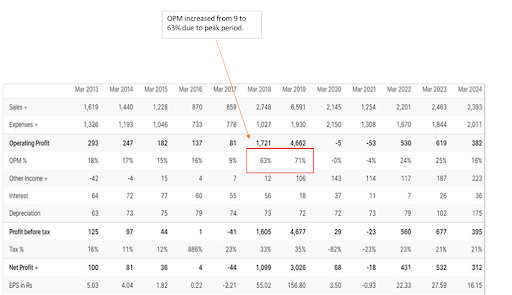

Take cases like graphite electrode manufacturers during supply shortages. Operating margins jumped from single digits to 60–70%. Earnings exploded. P/E ratios collapsed. But when supply normalised, margins vanished. Earnings fell. And the “cheap” stock wasn’t cheap anymore—it was priced for peak profits that never returned. Low P/E caused by peak earnings is not undervaluation. It’s an illusion.

A classic Indian example of this trap is HEG Ltd. In 2017–18, a global shortage of graphite electrodes driven largely by environmental shutdowns in China sent prices soaring. HEG’s operating margins exploded from single digits to over 60%, and profits followed. On the surface, the stock looked absurdly cheap, with the P/E ratio collapsing to seemingly “bargain” levels.

But those earnings were peak-cycle earnings, not normalised ones. As supply returned and prices cooled, margins reverted, profits fell sharply, and the low P/E that once looked attractive revealed itself as an illusion. Investors who bought purely on valuation learned a hard lesson about confusing cyclical peaks with sustainable profitability.

4.2. One-Time Gains Dressing Up Earnings

Sometimes earnings look strong—but only on paper due to:

4.2.1. Asset sales

4.2.2. Tax benefits

4.2.3. Accounting adjustments

These inflate net profit temporarily, dragging the P/E down. If you don’t strip out these one-offs, you’re valuing a business on earnings that won’t repeat. Cash flow usually exposes this lie faster than profit and loss statements.

4.3. Declining Businesses Wearing a Cheap Label

A shrinking business often looks cheap right before it becomes irrelevant.

4.3.1. Revenue stagnates.

4.3.2. Margins erode.

4.3.3. Competition intensifies.

4.3.4. The market senses this before the financials collapse—and prices the stock accordingly.

Cases like Café Coffee Day tell this story well. Once commanding high P/E multiples, the business slowly lost relevance. As profits declined and losses mounted, the P/E compressed—not because value emerged, but because confidence disappeared. A low P/E cannot revive a broken business model.

4.4. Debt Makes Cheap Stocks Dangerous

Debt changes everything. A leveraged company might look optically cheap until interest costs eat into earnings or refinancing becomes difficult.

During downturns, debt doesn’t just reduce upside—it threatens survival. Many energy and infrastructure stocks learned this lesson brutally during commodity crashes. A low P/E with high debt is not value—it’s leverage disguised as opportunity.

High P/E Can Fool You Too

Interestingly, the reverse also happens.

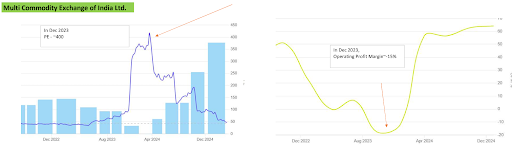

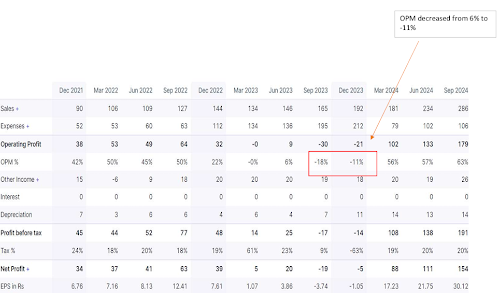

A high P/E doesn’t always mean overvaluation. Cyclical stocks during downturns often show absurd P/E ratios because earnings collapse temporarily. In such cases, high P/E reflects depressed earnings, not expensive prices. This is why relying on P/E alone — low or high without context leads to bad decisions. In FY23–24, MCX reported sharply lower profitability due to one-time technology transition costs and regulatory uncertainty.

Operating margins turned negative, earnings collapsed, and the P/E ratio shot up to eye-watering levels making the stock look outrageously expensive on the surface.

But the elevated P/E wasn’t a reflection of an overpriced stock; it was the result of temporarily depressed earnings. As operational stability returned and volumes normalised, profitability improved and the valuation started making far more sense in hindsight. A low P/E ratio isn’t an answer it’s a starting point.

Sometimes it reflects fear or temporary disruption, creating real opportunities. Other times, it hides peak-cycle earnings or structural decline, turning “cheap” stocks into value traps. Examples like HEG and MCX show that valuation only makes sense when viewed in context.

Good investing isn’t about buying low P/E stocks or avoiding high ones. It’s about understanding why a stock is priced the way it isand whether its earnings are sustainable. In the end, numbers don’t create value.

Durable businesses do.